Add Your Heading Text Here

Research Payments in 2026: A Trading‑Desk Playbook for the EU, UK, and US

The research‑payment landscape has entered a new phase. Since MiFID II reshaped the market in 2018, the EU and UK have moved in sharply different directions. The UK has embraced controlled optionality through PS24/9 and PS25/4, while the EU, long anchored to strict unbundling, is now introducing targeted but meaningful flexibility through the Listing Act and the forthcoming MiFID II Delegated Directive.

For global asset managers, this divergence is no longer a technical nuance. It is a structural shift that directly affects execution strategy, broker relationships, routing logic, and operational design. And for the first time in nearly a decade, Heads of Trading are back at the center of the research‑payment equation.

This article provides a trading‑desk‑focused view of where the EU and UK stand in 2026, how the Listing Act changes the EU narrative, and what Heads of Trading need to do next.

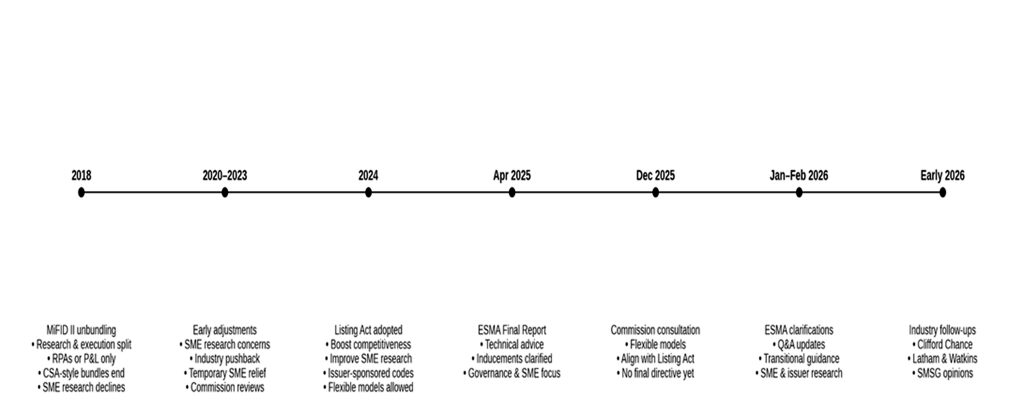

Timeline of EU Research‑Payment Reforms (2018 → 2026)

The above chart captures the EU’s journey from MiFID II’s 2018 unbundling mandate through the Listing Act, ESMA’s 2025 technical advice, and the 2026 clarifications. The EU has refined the regime, but the Listing Act introduces the first structural opening since 2018.

EU: Unbundling, Now with Listing Act Flexibility

Since 2018, the EU has treated research as a potential inducement, requiring firms to pay for it either from P&L or via a tightly governed Research Payment Account. For years, this created a rigid, fully unbundled environment that removed trading desks from research‑payment decisions.

The Listing Act changes that trajectory.

The Act introduces a more flexible framework for research, including:

- Removal of the €1bn SME threshold

- A formal structure for issuer‑sponsored research

- A clearer definition of what qualifies as “research”

- The first EU‑level opening for joint‑payment‑style models, subject to strict inducements safeguards

This is not a return to pre‑MiFID bundling. But it is the first time since 2018 that the EU has acknowledged the need for more pragmatic research‑payment pathways, particularly to support SME coverage and capital‑markets competitiveness.

ESMA’s 2025 technical advice and its 2026 clarifications reinforce this direction by tightening expectations around valuation, budgeting, governance, and disclosure. The forthcoming Delegated Directive will determine how far the EU goes, but the Listing Act has already shifted the center of gravity.

The EU is no longer “strictly unbundled with minor tweaks.” It is now “unbundled with controlled, Listing‑Act‑driven flexibility.”

UK: Optionality, but Within Guardrails

While the EU is cautiously opening the door, the UK has already walked through it. Through PS24/9 and PS25/4, the FCA has introduced a third payment option that allows firms to use a joint‑payment model for research and execution. The research charge must be separately identifiable, supported by clear governance and transparent disclosures.

This gives UK firms a pragmatic tool to re‑socialize research costs back into funds, improve access to global research providers, and simplify interactions with US broker‑dealers who cannot accept unbundled payments.

The UK now operates a flexible, three‑model regime, P&L, RPA, and joint payments, while the EU is transitioning from a rigid two‑model regime to a more flexible framework shaped by the Listing Act.

What Heads of Trading Need to Know; Quickly and Clearly

The UK already allows CSA‑style joint payments under FCA guardrails.

The EU is moving toward conditional joint‑payment flexibility through the Listing Act and the upcoming Delegated Directive, but the operational details will be tightly controlled.

The practical consequence is that global desks must now operate under two evolving regimes, not just two static ones. The UK’s model is live and operational; the EU’s model is emerging and will require careful interpretation.

This is not a compliance footnote. It is a shift that touches execution strategy, routing decisions, broker economics, and cross‑border consistency.

The Trading Desk Returns to the Center

MiFID II pushed trading out of the research‑payment business. The Listing Act and the UK’s joint‑payment model pull trading back in.

In the UK, joint payments are implemented at the point of execution, meaning the trading desk once again controls the levers that determine how research is funded. Broker selection, commission structures, and routing decisions now have direct research‑payment consequences.

In the EU, the Listing Act’s flexibility means trading desks will increasingly need to understand, and potentially implement, joint‑payment‑style workflows under strict inducements controls. Trading will not be as central as in the UK, but it will no longer be entirely removed.

The desk is becoming the operational nexus again.

What This Means for Execution Strategy and Broker Management

For UK‑domiciled accounts, joint payments can now be used to improve research access and liquidity. Brokers will reintroduce CSA frameworks and menu pricing, trading, research, and compliance will need to align on how joint payments are calculated and monitored.

For EU‑domiciled accounts, the Listing Act introduces the possibility of joint‑payment‑style models, but only within a tightly controlled inducements framework. Fully unbundled workflows remain the default until the Delegated Directive is finalized, but firms must prepare for a more flexible future.

The practical reality is that global trading desks must now run dual playbooks, one for the UK, one for the EU, and ensure that systems, billing, and MI can distinguish between the two.

Cross‑Border Consistency Without The Operational Disorganization

The divergence between the EU and UK regimes means that OMS/EMS configuration, broker billing, commission management, and reporting must all be able to slice activity by domicile, regime, payment model, broker, and strategy. Trading desks must be able to explain why the same strategy may fund research differently depending on where it is domiciled.

This is where the trading function becomes the control tower. It is the only place where execution quality, research access, and regulatory divergence converge into a coherent operating model.

How to Position This to Senior Stakeholders

The message is straightforward. The UK has moved first, deliberately reintroducing a controlled CSA‑style option to improve research access and competitiveness.

The EU is now moving, cautiously, through the Listing Act, which introduces the first meaningful flexibility since 2018.

And the firm needs optionality without chaos: a model where trading can support both regimes cleanly, transparently, and without compromising execution quality.

Where EU Research Payments Stand Today

The EU remains anchored in MiFID II’s philosophy, but the Listing Act marks the beginning of a more flexible era. The regime is still unbundled, but no longer rigid. ESMA’s 2025–2026 guidance reinforces governance expectations, and the Delegated Directive will determine how far the EU goes.

The EU is not adopting the UK model, but it is no longer standing still.

Final Word: Trading Is Back in the Control Tower

Since 2018, Heads of Trading were largely removed from research‑payment decisions. In 2026, the pendulum has swung back, in the UK decisively, and in the EU gradually through the Listing Act. Trading now sits at the intersection of execution quality, research access, broker economics, regulatory divergence, and client communication.